Written by Kristina Kananen

The average retiree in the United States receives $1,200 per month in Social Security income. It has dawned on state legislatures that it is not possible in our current economy for a retiree to survive with any sense of financial security on this income. Being loath to abandon these retirees, or to reinstitute the proverbial ‘Ice Flow’ as a solution, some states have begun to take steps to help workers ensure their own futures.

Currently there are three states with operating retirement programs: Oregon, California and Illinois. There are 9 other states that have enacted laws providing for various programs to facilitate retirement savings. Six of the programs are mandatory.

The businesses required to participate vary from state to state. For example, California requires businesses with 5 or more employees to participate if they do not currently have a plan, while Illinois requires businesses with 25 or more employees and in business for 2 or more years. Oregon, the first operational state- run plan, requires businesses with 1 or more employees for 18 weeks of the calendar year or where the payroll amounts to $1,000 or more to participate. For New Mexico, the requirement to participate in their plan covers any business physically located within the state.

Eight of the enacted plans offer, or will offer, an Auto IRA, while Washington offers a marketplace to facilitate offering a plan. New Mexico offers a hybrid of a marketplace and a Roth IRA. New York joins New Mexico in offering a Roth IRA.

Vermont and Massachusetts each offer a Multiple Employer Plan. But Massachusetts offers it for nonprofit employers with 20 or fewer employees.

Many of the bills introduced to state legislatures were introduced in 2015. These bills wandered around the legislature for years before seeing any action. They could languish in committees for years. However, interest seems to have increased in 2020 with more bills being introduced.

It takes at least two years from the date of enactment for a state-run program to open for participants. The process involves having committees in place to oversee the plans and selecting the investment products to offer, in essence, the creation of the bureaucracy to support the programs. New York’s program should have been active on 4/12/2020, 24 months after enactment.

The most disappointing are nine states who have not investigated a state-run program. Following in degree of disappointment are the 29 states who thought about a state-run program but have failed to legislate them. Many of these states formed task forces to investigate the need for a state-run program, as though they are unaware of the financial difficulties for retirees. Hawaii’s task force will sunset on 6/30/2021. Maine killed their bill on 11/16/2020. Mississippi did not let the bill out of committee. Nebraska has indefinitely postponed action on their bill.

While one may think that delaying or avoiding the establishment of a state-run program relieves the affected businesses of the cost, one is not thinking beyond today. As more employees enter retirement without financial security, the burden on society grows. Providing for retirement helps to ensure security and dignity for those entering retirement. And the goal is for all of us to enter retirement, so unless we drill the story of the grasshopper and the ant into children’s heads, we need to empower workers to save for themselves and take more control of their futures.

While state-run programs provide some hope for future retirees, one must ask if the creation of a new state bureaucracy and the mandating of employer participation is the best answer to the coming financial strain.

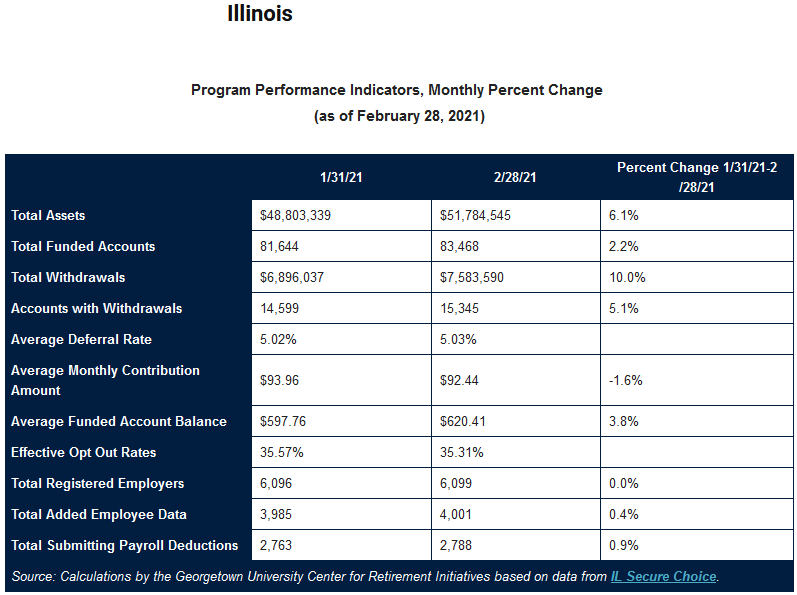

The delay in providing the state-run programs gives the private retirement plan industry the opportunity to establish retirement plans for employers before they are subject to mandated programs. The market is huge as can be seen from a Monthly State Program Performance Data & Trends report prepared by the Center for Retirement Initiatives at Georgetown University for the 3 active states below.

The key is finding programs or products that meet all of the needs of the employers. Hopefully, the PEPs, MEPs and GofPs established under the Secure Act will go a long way to meeting those needs. However, Congress gave us the Simple IRAs and Simple 401(k)s as well as SEPs in the past which all represent low administrative costs without a flood of eligible adopters getting on board.

It will take a dedicated, and unique, approach for financial advisors to be able to reach the small employers who should be their target market. Digital marketing as well as relationship building with accountants and attorneys will probably form the basis for seeing that more employees are able to save and provide for their own futures.