State mandated plans are the result of well intentioned state officials or representatives understanding the yawning retirement readiness gap facing many of their citizens. But missing out on a few details. In this article we will explore what they are missing and some different options that might work well for you and your business. We will also preform an in depth comparison between plans.

State mandated plans are mandatory for employers who has not yet provided a retirement plan to their employees. Each state has a different minimum threshold – right now Illinois is for employers with more than 15 employees and it drops to more than 5 employees in 2023 – that requires employers to either have a plan or enroll their employees in the state mandated plan. The choice is up to them.

This article aims to educate you on the options you do have and what the best plan is for your business. There is a lot to consider when choosing a plan but we will do our best to simplify it as much as possible and provide you with an easy decision. Let’s jump in!

Why Are States Doing This?

Why are states having to do this? Here’s one article discussing it. Essentially over 50% of the over age 30 workforce are projected to be unable to retire when they’re old enough. If employees aren’t leaving the workforce because they can’t afford to, it makes it hard for new employees to be hired. The states are doing what they can to – gently or otherwise – to encourage employers to help reduce the retirement readiness gap.

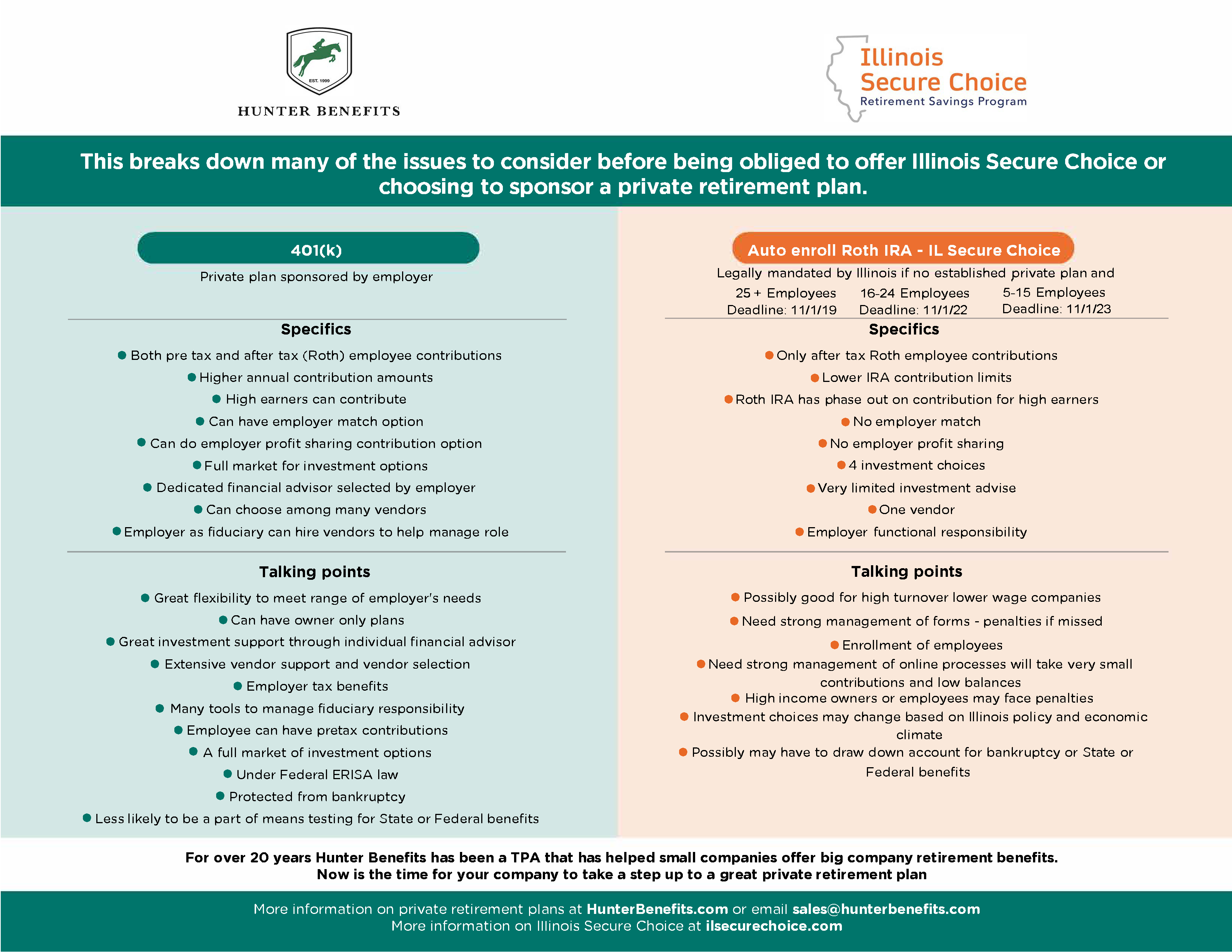

Pros Of A State Mandated Plan

- States sponsoring mandated plans have recognized the retirement gap and are doing something to help reduce the gap.

- Limited employee notice requirements.

- No annual tax filing.

- No individual employer document requirements.

Cons Of A State Mandated Plan

- Only Roth contributions. No pre-tax option. If an employee is not eligible for Roth contributions, the employee must pay a penalty to correct the contribution.

- The individual State is the Plan Sponsor and usually is not able to provide any help or guidance to the employees enrolled in the plan.

- Total contribution amounts are very limited.

- Employer contributions aren’t allowed.

- As the accounts are Roth IRAs, they can’t be rolled into an employer’s 401(k) plan. Only into other IRSs.

- Limited investment selections.

- Generally no help understanding the investment options.

Pros Of Employer Sponsored Plans

- Many more investment options.

- Pre-tax contributions as well as after tax Roth.

- Employer contributions are possible.

- Can provide sufficient income at retirement.

- Is seen as a new employee recruiting tool – for a potential employee to consider working for you, some kind of retirement plan needs to be in place.

Cons Of Employer Sponsored Plans

- Many more investment options.

- Highly compensated employee contributions are limited by contributions for the rank and file.

- Unless a company can do all the compliance work themselves, the Plan Sponsor will need to pay for outside help.

- The Plan Sponsors are legally accountable for what happens in the Plan.

- Plan Sponsors have an obligation to ensure that Participants are provided with certain notices at least annually.

How To Choose The Best Plan For You

For the employer who suddenly finds themselves subject to their state’s mandated plan and haven’t had a chance to set up their own sponsored – start with the state plan and start researching other alternatives. Below is a listing of the benefits of each of the three main alternatives.

State Mandated Retirement Plan Benefits:

- No employer contributions

- No compliance fees

- Limited notification obligations

- Not acting as a fiduciary

Simple IRA Retirement Plan Benefits:

- No compliance fees

- No discrimination testing obligations

- No fiduciary obligations

401(k) Retirement Plan Benefits:

- Can be designed to not require any employer contributions

- Choose between pre-tax and after-tax Roth contributions

- Participant loan availability

- Employer contribution vesting options

- Much larger employee contribution limits

- Much larger employer contribution limits

- Can be coordinated with a Cash Balance Plan

Unbundled vs Bundled 401(k) plans

After you have had a chance to review the different benefits, the next task is to review what you as an employer want from a plan, regardless of what regulations are telling you to do. If you want an option where you don’t have to make an employer contribution, your choice is between the state plan and a 401(k). If you want an option where you can’t make large contributions for yourself but are okay with a nominal contribution for your employees, you’re probably looking at a Simple IRA. But if you want maximum flexibility and maximum contribution amounts, the only choice is to sponsor your own 401(k) plan.